Payments should be free, That's when financial services will include everyone.

Did You Know that When money moves you pay, when it does not move you pay, if you want it fast you pay and if you want it to delay again you pay fees for that.

WhatsApp has more users than all mobile money combined: But why?

Globally WhatsApp has over 2.5 billion monthly active users, while mobile money services have only 435 million, The main reason? Using WhatsApp is free, mobile money isn't. In essence, the free-to-use model of WhatsApp and Youtube significantly lowers the barriers to entry and increases its daily usage, leading to its vast active user base. In contrast, mobile money services, despite their critical role in financial inclusion, face hurdles due to the costs associated with their use, resulting in relatively lower usage and that hinders experimenting with more sticky products.

Is there anyone who can explain to me why there is more Youtube users in the world, I mean 2 billion more users than all mobile money operators combined?

In countries where mobile phone penetration is high but digital financial inclusion is still low, innovative approaches are essential. Mobile money and peer-to-peer payments have the potential to be the engine of financial inclusion, especially if some frequent payment services are made free. This strategy can significantly boost participation, bringing more people and money into the digital economy. By eliminating fees for certain payments, we can incentivise banks, mobile money operators, and fintech companies to innovate and invest beyond payments fees.

Millions of customers will go back to cash if charges increase even a little.

In one year after levies increased cost of mobile money payments in Tanzania M-pesa lost about $50 million in Revenues, this shows you how sensitive customers are when it comes to payment fees. The same year, M-pesa users fell from 7.8 million to 6.5 Million as a result of payment fees increase, wiping out years of efforts in sales, retention and financial inclusion.

“By eliminating fees for frequent payments we lower the barrier to participation in digital financial services, we can incentivise mobile money, and fintechs to experiment with new models beyond payments fees, That way everyone wins in the long run, there’s more users, more revenues”

Payment fees is a top reason for low usage and low activity across markets.

In this study, GSMA, which is very respected in the field of mobile money, notices that only 26% of people use mobile money monthly and transaction fees is one of the main reason there is not much activity on mobile money and people choose to use cash in Tanzania, Kenya, India and Pakistan. My best guess is that activity levels would double if payments charges were abolished in most transaction categories.

In Tanzania, mobile money and peer-to-peer payments hold immense potential to transform financial transactions and drive economic growth. With 90% of the population having access to mobile phones, the infrastructure for digital payments is already in place. However, the usage of mobile money for regular transactions remains low. Only 1% of airtime is paid for via mobile, 93% of groceries are still bought with cash, and just 3% of people have title deeds for their land. To address these challenges and promote financial and digital inclusion, we propose making key payment services free. This strategy can attract more users and capital incentivising banks, mobile money operators, and fintechs to innovate and invest beyond payment models.

Mobile money is further behind, with 60% of its customers claiming the high cost of service to be a key concern for low usage of the service. This is concerning since mobile money is the most penetrated financial service. This particularly causes low frequency of service usage for lower-income earners in rural areas, as it was observed by FinsCope Tanzania 2023

The importance of free payments: Payments are the engine of financial inclusion. By eliminating fees for essential payment services, we can encourage broader participation in the digital economy. Here's how free payments can revolutionise financial inclusion in Tanzania and beyond:

Increased Adoption and Usage: Free payments will lower the barrier to entry for many individuals, encouraging them to use mobile money for everyday transactions. This can lead to a significant shift from cash-based to digital transactions, fostering a more inclusive financial environment.

Economic Empowerment: Making payments free can empower more people to save, invest, and borrow money. This financial empowerment can lead to greater economic stability and growth, as individuals can better manage their finances and plan for the future.

Encouraging Innovation: By starving revenues from traditional payment fees, financial institutions will be motivated to explore new business models and revenue streams. This can lead to innovative solutions that further enhance financial inclusion and cater to the unique needs of the Tanzanian market.

Not every type of payments, So What can actually be free?

Mobile money and peer-to-peer payments are revolutionising financial transactions, offering unmatched convenience and accessibility. To drive further financial inclusion, we propose making five key payment services free. This move not only benefits consumers but also demonstrates that such innovations are feasible and can become industry standards. This discussion explores these five payment services—peer-to-peer payments, intra-provider transactions, ATM and agent withdrawals, savings, investments, and loan repayments—and their potential impact on the financial sector.

Peer to Peer Payments - If one does it well, the rest will loose customers because it is the best use case for mobile money, it may also start like “for accounts of the same person” in different banks and mobile money operators then accounts of your family and friends, we may also think of lower P2P values first.

Payments within same provider - Payments within the same mobile money operator, AirtelMoney has done this in Tanzania and Rwanda and a lot of banks are doing so, If all mobile operators do that then it will become an industry standard. Safaricom did it during covid19 and everyone was happy in Kenya.

One withdrawal a day for ATMs and Agents - Mpesa and TigoPesa are already doing this for their merchants in Tanzania with lipakwasimu/LipaNamba merchants, so we know it is practically possible. This will kill the “ya kutoa or ya kutolea” surcharge that merchants put on customers making it even pricier.

Savings & Investments - Don’t charge when I move money to save or invest, I need to be able to get more money not lose money. For innovators this is also a major challenge that troubled Tunzaa and TemboPlus original savings product which were supposed to work well with mobile money and cards both of which are charged 1-3% the amount when you save and when you withdrawal.

Loan repayments: I’m paying 20% to the lender as interest and fees and I also have to pay 3% to actually send money to them every month. What kind of world are we living in guys come on: Okey then I am going to choose not to send haha!

“I wish payments were free, that way the barrier to digital payments becomes very low and everyone can participate, Think about it, if payments were free there could be more innovation beyond just moving money. That could be a good way of incentivising those who go further.”

So what could we charge for, now we are not charging for payments?

You can charge for B2B, B2C, C2G as well as merchant & biller payments, There’s a lot more to charge for around services beyond payments but think outside the box of payments fees, Think of the below and expand the pie:

Create and grow new revenue lines: Now you will truly innovate and actively experiment to discover new revenues streams which at the end benefits everyone. The beauty of this is once you discover or stumble upon something valuable then you have the first mover advantage to capitalise on.

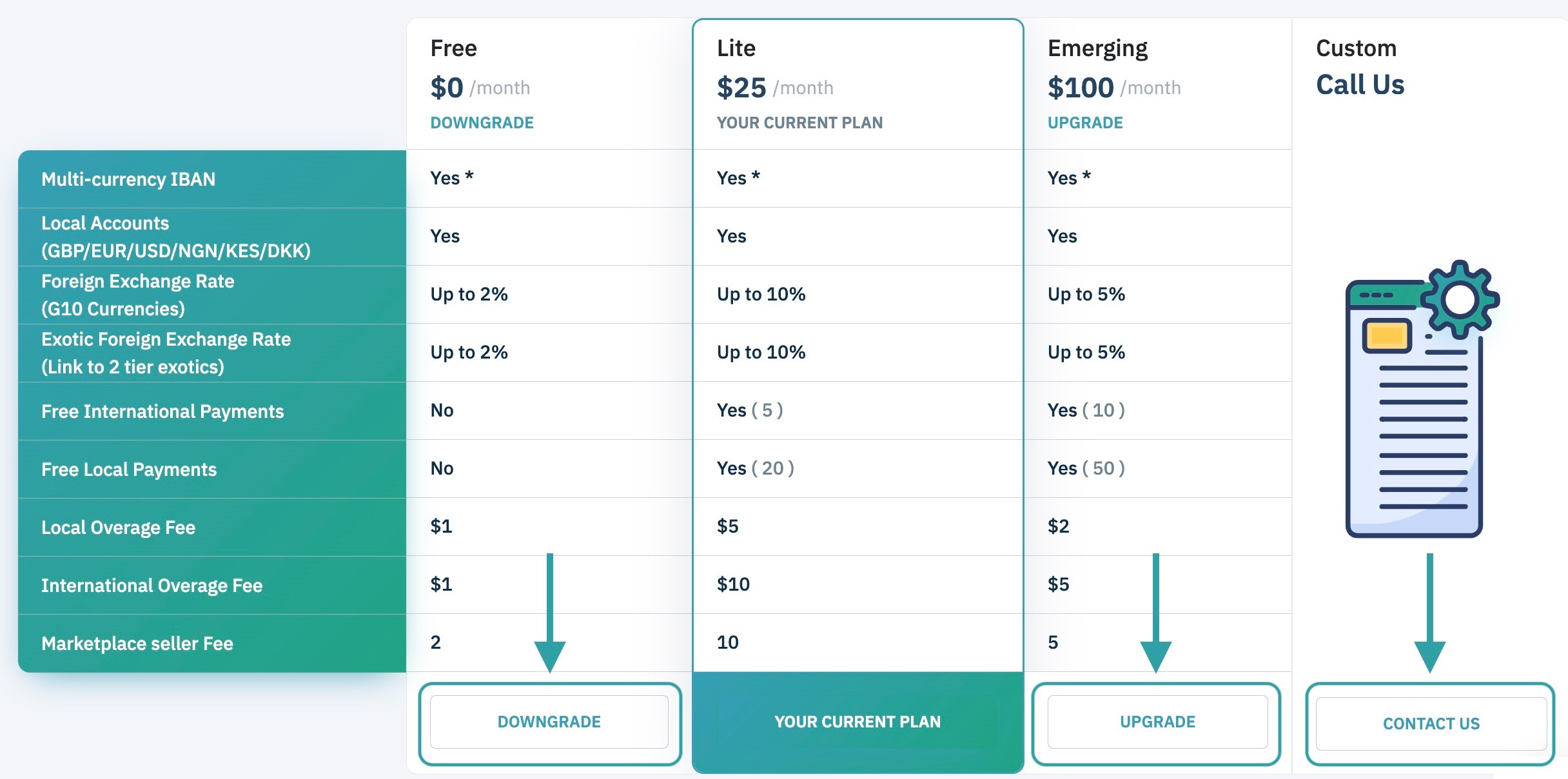

Change to subscription business model: Think of changing your business model from transactional fees to subscriptions like annual subscription, monthly and weekly. Think of Netflix for a combined payments services experience.

Try freemium business model: Think of changing your business model from transactional fees to freemium model where payments are free but premium services are paid for. Think of Spotify for a combined payments services experience.

Be the Google of Payments: Think of changing your business model from transactional fees to ad supported model where moist services are paid by advertisers, sponsors & grantors.

Sell Bundles of Payments Experience: Think of changing your business model from transactional fees to bundles similar to airtime and data bundles like telecom companies. Monthly, Weekly, Daily or Limited bundles for a season.

“Tanzania boasts a 90% mobile phone penetration, Although shockingly Only 7% of airtime is paid via mobile phone, 93% of groceries are still bought with cash.”

Conclusion: While making certain payment services free can drive financial inclusion, there are still viable revenue opportunities. Providers can still charge for B2B, B2C, C2G, and merchant payments all of which are fast growing sub segments, we need more inclusion there (not in p2p) so let them push that, that way we all win. Additionally, innovative business models such as subscriptions, freemium services, ad-supported models, and bundled payment experiences can replace traditional transaction fees. By adopting these approaches, financial service providers can continue to thrive and innovate, ensuring a sustainable future in the evolving digital financial inclusion that includes everyone and leaves no one behind.

Call to Action: Others who are interested on this should probably crunch the numbers to extrapolate how many people would actually use mobile money actively if payment fees were abolished in Tanzania, Kenya, Uganda and Beyond.

Great article, Reuben!

Great read! Eye-opening.