Main API providers for fintechs, challenger banks and neobanks in Tanzania.

Building Blocks: A list of reputable API providers you may need to work with to launch and scale a fintech in Tanzania.

I Reuben Mwatosya strongly believe that the number of fintechs and their unmatched impact in financial inclusion in markets like the US and the UK has mainly been powered by the existence of fintech infrastructure players like Synctera Synapse Modulr ComplyAdvantage Veriff Plaid Column Marqeta and many more I’ve not mentioned which powers super fintechs like Revolut, N26, Mercury Venmo Square Stripe Uber and Shopify --- I know the last two may not make sense, hold that thought !

Like many African countries, Tanzania need more API infrastructure players to power fintech and startups, John Haule wrote about API service providers he posted it on Linkedin and I got inspired to write a little further on the same subject: 🇹🇿

Tanzania is an incredible place for fintechs because it has a bigger population, a fairly more competitive market and the country seats right in the centre as a regional trading hub for 8 neighbour countries.

In the dynamic realm of Tanzanian FinTech and elsewhere in the world, the foundation for revolutionary change lies in its building blocks. These essential components are reshaping the financial landscape, driving innovation, and fostering inclusive growth across the nation. Let's delve into the key pillars shaping Tanzanian FinTech infrastructure:

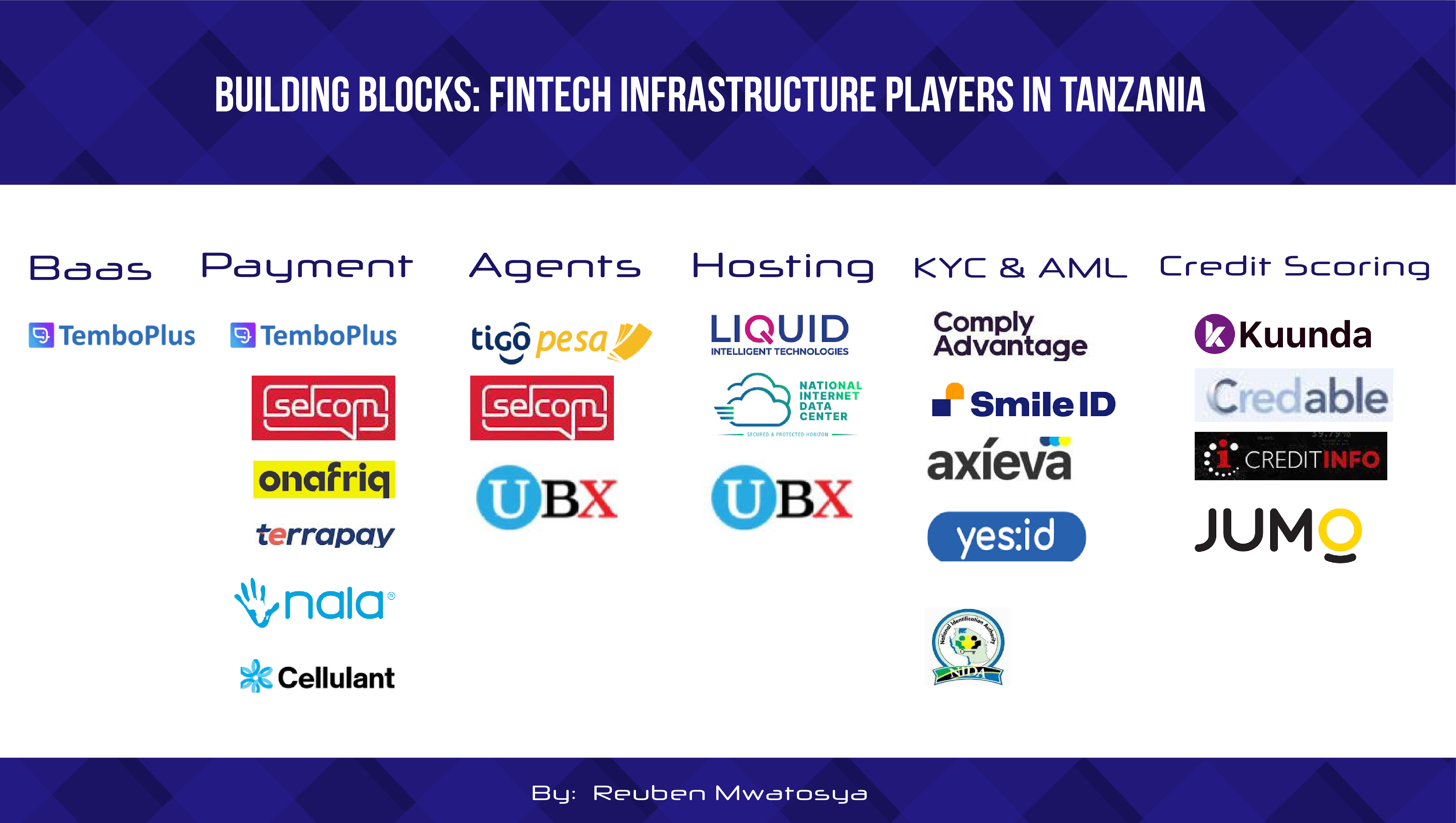

The building blocks might be APIs for data sharing, payments, remittances, KYC verifications, AML checks, Credit scoring, access to merchants, agents and customers, It can also be a partnership to allow you to use ATMs, BINs for debit cards, Local data hosting as well as APIs to issue bank accounts and wallets.

🌟 "Every company is going to be a FinTech company. The only question is whether they know it or not." - Angela Strange 🚀

Whether you are trying to offer a digital loan or a simple embedded virtual card in you budgeting app in Tanzania, The below are the building blocks that founders and non fintech companies can use to quickly launch financial services in Tanzania. This excludes fintechs that are building infrastructure for their exclusive use e.g Ramani.io Laina Finance, it focuses on those players who build for other businesses, banks, telcos and fintechs.

Banking as a service APIs: A leading Tanzania's BAAS infrastructure player is revolutionising traditional banking services by offering seamless digital banking solutions accessible through mobile devices. They provide all sorts of APIs and SDKs allowing for digital bank accounts, wallets, payments, collections, cards and eKYC. The key player in that space is Tembo and probably the only full service player used by tens of SaaS companies, fintechs, IMTOs and neobanks.

ATMs: Anchoring financial accessibility are automated teller machines (ATMs). Beyond dispensing cash, modern ATMs offer a gateway to a spectrum of banking services. With advanced features like cardless transactions and biometric authentication, FinTech-powered ATMs are revolutionising financial access, especially in underserved regions. Leading player in shared ATM network include UBX Tanzania Limited and NMB Bank Plc which together they represent a wider network of ATMs in thousands of places.

Cards: The proliferation of prepaid cards, debit cards, and virtual cards solutions is transforming retail transactions in a big way, so if you are trying to add that card feature you should talk to the major players like Onafriq Selcom Tanzania and Umoja Switch (UBX Tanzania)

Agents: In the realm of FinTech, agents serve as pivotal intermediaries, bridging the gap between traditional banking infrastructure and underserved populations. These agents, authorized by financial institutions or FinTech companies, facilitate essential financial services such as cash deposits and withdrawals, bill payments, and account openings. Key players include UBX Tanzania Limited Selcom Tanzania and most recently Tigo Tanzania Plc has opened up their network of 200,000 agents to banks and probably fintechs.

Payments aggregation: It is at the heart of typical fintech products, offering payments aggregation services that consolidate various payment channels, preferences, enhancing efficiency and accessibility for businesses and consumers. Leading players in this would include Tembo Cellulant Selcom Tanzania PesaPal

Data hosting and Cloud services: The backbone of FinTech innovation lies in robust cloud and data hosting infrastructure as well as local data compliance. By harnessing cloud computing, Tanzanian FinTech firms can securely store and process vast amounts of data. This scalability fosters agility, accelerates innovation, and ensures compliance with regulatory standards, laying the groundwork for sustainable growth. Most famous players includes UBX Tanzania Limited Liquid Intelligent Technologies.

KYC and AML screening: Integral to regulatory compliance within the FinTech industry. KYC involve verifying the identity of customers and assessing their suitability and safety. AML measures focus on preventing and detecting illegal activities like money laundering and terrorist financing. By implementing robust KYC and AML processes, FinTech can mitigate risks and comply with regulations, and uphold the integrity of the financial system, fostering trust and confidence among customers and stakeholders. Major players like IDTech Holdings Smile ID Axieva.

Credit Scoring: In the quest for financial inclusion, credit scoring algorithms and digital platforms are pivotal. These tools enable real-time credit assessment, empowering lenders to extend credit to underserved segments of society. Moreover, balance sheet management tools and financial analytics platforms are optimising decision-making processes, fostering financial resilience, and driving sustainable growth. Major players like CreditInfo Kuunda Credable JUMO have been working with mobile money operators and banks to launch successful financial products such as M-kopa and Songesha which are super hits.

Balance sheet providers: Balance sheet providers, often licensed lenders such as banks, play a pivotal role in the financial ecosystem by offering comprehensive financial services beyond mere lending. These entities usually licensed and regulated by relevant authorities. By leveraging their expertise and resources, licensed lenders ensure prudent risk management, facilitate capital allocation, and support the growth. Most famous Balance sheet providers working with fintechs and mobile money operators includes NCBA, TCB bank, FINCA, NMB Bank KCB Bank and CRDB bank

Remittances and international payments: The FinTech landscape in Tanzania is facilitating cost-effective and efficient cross-border remittance solutions, enabling individuals to send and receive money from abroad with reduced fees and faster processing times. Leveraging digital platforms and blockchain technology, FinTech companies are disrupting traditional remittance channels, offering competitive exchange rates and enhanced transparency in transactions. Major players like Tembo Onafriq Selcom Tanzania TerraPay and NALA which is joining the pack with rafiki.api proposition.

Merchants and Individual Customers: Major players like Selcom Tanzania Vodacom Airtel Tigo they have provided APIs for innovative fintechs to use or just access their customers including agents, individual and merchants. In the past they have rented their merchants, customers and agents to digital lenders, fintechs, neobanks or banks.

In conclusion, guided by Angela Strange's foresight, Tanzanian FinTech infrastructure emerges as the cornerstone of a future where every company is a FinTech company and mega fintech player will emerge as the years go by. These building blocks are not just components; they are catalysts for change, driving innovation, inclusion, and empowerment. As these pillars continue to evolve and intertwine, they lay the groundwork for a brighter financial future, where every Tanzanian has the opportunity to thrive.